Dive into the Dedaub blog for expert insights on smart contract security and blockchain innovation. Explore the latest advancements in the Ethereum ecosystem, including program analysis and DeFi exploits, through concise, expert-driven content designed for developers and blockchain enthusiasts.

Smart contracts on the Ethereum blockchain greatly benefit from cutting-edge analysis techniques and pose significant challenges. A primary challenge is the extremely low-level representation of deployed contracts. We present Elipmoc, a decompiler for the next generation of smart contract analyses. Elipmoc is an evolution of Gigahorse, the top research decompiler, dramatically improving over it and over other state-of-the-art tools, by employing several high-precision techniques and making them scalable. Among these techniques are a new kind of context sensitivity (termed “transactional sensitivity”) that provides a more effective static abstraction of distinct dynamic executions; a path-sensitive (yet scalable, through path merging) algorithm for inference of function arguments and returns; and a fully context sensitive private function reconstruction process. As a result, smart contract security analyses and reverse-engineering tools built on top of Elipmoc achieve high scalability, precision and completeness.

Elipmoc improves over all notable past decompilers, including its predecessor, Gigahorse, and the state-of-the-art industrial tool, Panoramix, integrated into the primary Ethereum blockchain explorer, Etherscan. Elipmoc produces decompiled contracts with fully resolved operands at a rate of 99.5% (compared to 62.8% for Gigahorse), and achieves much higher completeness in code decompilation than Panoramix—e.g., up to 67% more coverage of external call statements—while being over 5x faster. Elipmoc has been the enabler for recent (independent) discoveries of several exploitable vulnerabilities on popular protocols, over funds in the many millions of dollars.

The Dedaub Watchdog is a technology-driven continuous auditing service for smart contracts.

What does this even mean? “Technology-driven”? Is this a buzzword for “automated”? Do you mean I should trust a bot for my security? (You should never trust security to just automated solutions!) And “auditing” means manual inspection, right? Is this really just auditing with tools?

Let’s answer these questions and a few more…

Watchdog brings together four major elements for smart contract security:

automated, deep static analysis of contract code

dynamic monitoring of a protocol (all interacting/newly deployed contracts, current on-chain state, past and current transactions)

statistical learning over code patterns in all contracts ever deployed in EVM networks (Ethereum, BSC, Avalanche, Fantom, Polygon, …)

human inspection of warnings raised.

All continuously updated: if a new vulnerability is discovered, the most natural question is “am I affected?” Watchdog queries are updated to detect this and warn you.

At Dedaub, we have audited thousands of smart contracts, comprising tens of high-value DeFi protocols, numerous libraries and Dapps. Our customers include the Ethereum Foundation, Chainlink, Immunefi, Nexus Mutual, Liquity, DeFi Saver, Yearn, Perpetual, and many more. Since 2018, we’ve been operating contract-library, which continuously decompiles all smart contracts deployed on Ethereum (plus testnets, Polygon, and soon a lot more).

The Watchdog service brings together all our expertise: it captures much of the experience from years of smart contract auditing as highly-precise static analyses. It is an analysis service that goes far beyond the usual linters for mostly-ignorable coding issues. It finds real issues, with high fidelity/precision.

So, what does Watchdog analyze for? There are around 80 analyses at the time of writing, in mid-2022. By the time you read this, there will likely be several more. Here are a few important ones for illustration.

DeFi-specific analyses

Is there a swap action on a DEX (Uniswap, Sushiswap, etc.) that can be attacker-controlled, with respect to token, timing manipulation, or expected returned amount? Such analyses of the contract code are particularly important to combine with the current state of the blockchain (e.g., liquidity in liquidity pools) for high-value vulnerability warnings. More on that in our “dynamic monitoring”, later.

Are there callbacks from popular DeFi protocols (e.g., flash loans) that are insufficiently guarded and can trigger sensitive protocol actions?

Are there protection schemes in major protocols (e.g., Maker) that are used incorrectly (or, more typically, with subtle assumptions that may not hold in the client contract code)?

Cryptographic/permission analyses

Does a permit check all sensitive arguments?

Does cryptographic signing follow good practices, such as including the chain id in the signed data? (If not, is the same contract also deployed on testnets/other chains, so that replay attacks are likely?)

Can an untrusted user control (“taint”) the arguments of highly sensitive operations, such as approve, transfer, or transferFrom? If so, does the contract have actual balances that are vulnerable?

Statistical analyses

Compare the contract’s external API calls to the same API calls over the entire corpus of deployed contracts. Does the contract do something unusual? E.g., does it allow an external caller to control, say, the second argument of the call, whereas the majority of other contracts that make the same call do not allow such manipulation? Such generic, statistical inferences capture a vast array of possible vulnerabilities. These include some we have discussed above: e.g., does the contract use Uniswap, Maker, Curve, and other major protocols correctly? But statistical observations also capture many unknown vulnerabilities, use of less-known protocols, future patterns to arise, etc.

Conventional analyses

Watchdog certainly analyzes for well-known issues, such as overflow, reentrancy, unbounded loops, wrong use of blockhash entropy, delegatecalls that can be controlled by attackers, etc. The challenge is to make such analyses precise. Our technology does exactly that.

Yet-unknown vulnerabilities

We continuously study every new vulnerability/attack that sees the light of day, and try to derive analyses to add to Watchdog to detect (and possibly generalize) the same vulnerability in different contracts.

Monitoring

No matter how good a code analysis is, it will nearly never become “high-value” on its own. Most of the above analyses become actionable only when combined with the current state of the blockchain(s). We already snuck in a couple of examples earlier. An analysis that checks if a contract allows an untrusted caller to do a transferFrom of other accounts’ funds is much more important for contracts that have allowances from other accounts. A warning that anyone can cause a swap of funds held in the contract is much more important if the contract has sizeable holdings, so that the swap is profitable after tilting the AMM pool. An analysis that checks that a signed message does not include a chain id is much more important for contracts that are found to be deployed on multiple chains.

Combining analysis warnings with the on-chain state of the contract (and of other contracts it interacts with) is precisely the goal of Watchdog, and how it can focus on high-promise, high-value vulnerabilities.

Inspection

Automation is never the final answer for security. Security threats exist exactly because they can arise at so many levels of abstraction: from the logical, protocol, financial level, all the way down to omitting a single token in the code. Only human intelligence can offer enough versatility to recognize the potential for sneaky attacks.

This is why Watchdog is a technology-driven continuous auditing service. It can issue warnings that focus a human’s attention to the most promising parts of the code. By inspecting warnings, the human auditor can determine whether they are likely actionable and escalate to protocol maintainers.

We call Watchdog auditors “custodians”. The custodian of a protocol is not just a code auditor, but the go-to person for all warnings, all contacts to Dedaub and to other security personnel. By subscribing to Watchdog, a project gets its designated custodian who monitors warnings, knows the contact points and how to escalate reports, coordinates with any incident response team (either in place, or ad hoc, either external, or as part of Dedaub services), and ultimately advises on the project’s security needs.

In terms of software alone, Watchdog integrates two ideas to help a custodian inspect and prioritize warnings:

The concept of protocols: all contracts monitored are grouped into protocols, based on deployers and interactions. Any new contracts that get deployed are automatically grouped into their protocol and monitored. Reports and watchlists are easy to define to match the project’s needs.

Flexibility in the amount of warnings issued: Watchdog comes with different levels of service. The minimum level gets roughly a couple of hours per week of a custodian’s time. At this level, the custodian will likely only issue the highest-confidence warnings and inspect them very quickly. The next level of support, intended to be the middle-of-the-road offering, covers roughly two auditor-days per month. At that level, the custodian can spend significant time, at least every couple of weeks, to inspect a broader range of warnings. Watchdog supports this configurability seamlessly: it lets the custodian select warning kinds and mix them with many filters, to produce an inspection set that is optimal for covering in a given amount of time.

Contact Us … Soon

The Watchdog service has already had a handful of early institutional adopters (such as Nexus Mutual and the Fantom blockchain, both securing multiple protocols). We are currently enhancing our infrastructure and organizational capability, to launch Watchdog to broad availability (for individual protocols and not just institutional clients) by the end of 2022. You will be able to make inquiries and book a demo or live technical presentation with our team on the Dedaub Watchdog page.

On Jan. 10 we made a major vulnerability disclosure to the Multichain project (formerly “AnySwap”). Multichain has made a public announcement that focuses on the impact on their clients and mitigation. The announcement was followed by attacks and a flashbots war. The total value of funds currently lost is around 0.5% of those directly exposed initially.

We will document the attacks and defense in a separate chronology, to be published after the threat is fully mitigated. This brief writeup instead intends to illustrate the technical elements of the vulnerability, i.e., the attack vector.

The attack vector is, to our knowledge, novel. The Solidity/EVM developer and security community should be aware of the threat.

In the particular case of Multichain contracts, the attack vector led to two separate, major vulnerabilities, one mainly in the WETH (“Wrapped ETH”) liquidity vault contract (an instance of AnyswapV5ERC20) and one in the router contract (AnyswapV4Router) that forwards tokens to other chains. The threat was enormous and multi-faceted — almost “as big as it gets” for a single protocol:

On Ethereum alone, $431M in WETH would be stolen in a single, direct transaction, from just 3 victim accounts. We demonstrated this on a local fork before the disclosure. (Balances and valuations are as of the time of original writing of this explanation, on Jan.12. The main would-be victim account, the AnySwap Fantom Bridge, was holding over $367M by itself. At the time of publication of this article, the same contract held $1.2B.)

The same contracts have been deployed for different tokens and on several blockchains, including Polygon, BSC, Avalanche, Fantom. (Liquidity contracts for other wrapped native tokens, such as WBNB, WAVAX, WMATIC are also vulnerable.) The risk on these other networks was later estimated at around $40M.

The main would-be victim account, the AnySwap Fantom Bridge, escrows tokens that have moved to the Fantom blockchain. This means that an attacker could move any sum to Fantom and then steal it back on Ethereum, together with the current $367M of the bridge (and the many tens of millions from other victims, separately). The moved tokens would still be alive (and valuable) in Fantom, or anywhere else they have since moved to. This makes the potential impact of the attack theoretically unbounded (“infinite”): any amount “invested” can be doubled, in addition to the $431M amount stolen from Ethereum victims and however much on other chains.

Close to 5000 different accounts had given infinite approval for WETH to the vulnerable contracts (on Ethereum). This number has since dropped substantially(especially among accounts with holdings), but there is still a threat: any WETH these accounts ever acquire is vulnerable, until approvals are revoked.

Given the above, the potential practical impact (had the vulnerability been fully exploited) is arguably in the billion-dollar range. This would have been one of the largest hacks ever—given the theoretically unbounded threat, we are not getting into more detailed comparisons.

Phantom Functions | Attack Vector

Briefly:

Callers should not rely on permit reverting for arbitrary tokens.

The call token.permit(...) never reverts for tokens that

do not implement permit

have a (non-reverting) fallback function.

Most notably, WETH — the ERC-20 representation of ETH — is one such token.

We call this pattern a phantom function— e.g., we say “WETH has a phantom permit” or “permit is a phantom function for the WETH contract”. A contract with a phantom function does not really define the function but accepts any call to it without reverting. On Ethereum, other high-valuation tokens with a phantom permit are BNB and HEX. Native-equivalent tokens on other chains (e.g., WBNB, WAVAX) are likely to also exhibit a phantom permit.

In more detail:

Smart contracts in Solidity can contain a fallback function. This is the code to be called when any function f() is invoked on a contract but the contract does not define f().

In current Solidity, fallback functions are rather exotic functionality. In older versions of Solidity, however, including fallback functions was common, because the fallback function was also the code to call when the contract received ETH. (In newer Solidity versions, an explicit receive function is used instead.) In fact, the fallback function used to be nameless: just function(). For instance, the WETH contract contains fallback functionality defined as follows:

function() public payable {

deposit();

}

function deposit() public payable {

balanceOf[msg.sender] += msg.value;

Deposit(msg.sender, msg.value);

}

This function is called when receiving ETH (and just deposits it, to mint wrapped ETH with it) but, crucially, is also called when an undefined function is invoked on the WETH contract.

The problem is, what if the undefined function is relied upon for performing important security checks?

In the case of AnySwap/MultiChain code, the simplest vulnerable contract contains code such as:

This means that the regular deposit path (function deposit) transfers money from the external caller (msg.sender) to this contract, which needs to have been approved as a spender. This deposit action is always safe, but it lulls clients into a false sense of security: they approve the contract to transfer their money, because they are certain that it will only happen when they initiate the call, i.e., they are the msg.sender.

The second path to depositing funds, function depositWithPermit, however, allows depositing funds belonging to someone else (target), as long as the permit call succeeds.

For ERC-20 tokens that support it, permit is an alternative to the standard approve call: it allows an off-chain secure signature to be used to register an allowance. The permitter is approving the beneficiary to spend their money, by signing the permit request. The permit approach has several advantages: there is no need for a separate transaction (spending gas) to approve a spender, allowances have a deadline, transfers can be batched, and more.

The problem in this case, as discussed earlier, is that the WETH token has a phantom permit, so the call to it is a non-failing no-op. Still, this should be fine, right? How can a no-op hurt? The permit did not take place, so no approval/allowance to spend the target’s money should exist.

Unfortunately, however, the contract already has the approvals of all clients that have ever used the first deposit path (function deposit)!

All WETH of all such clients can be stolen, by a mere depositWithPermit followed by a withdraw call. (To avoid front-running, an attacker might split these two into different transactions, so that the gain is not immediately apparent.)

Phantom Functions | Notes:

Two separate vulnerabilities are based on the above attack vector. The first was outlined above. The second, on AnySwap router contracts, is a little harder to exploit — requires impersonating a token of a specific kind. We do not illustrate in detail because the purpose of this quick writeup is to inform the community of the attack vector, rather than to illustrate the specifics of an attack.

We have exhaustively searched for other services with similar vulnerable code and exposure. This includes vulnerable contracts with approvals over tokens with phantom permits other than WETH . Although we have found other instances of the vulnerable code patterns, the contracts currently have very low or zero approvals on Ethereum. (This kind of research is exactly what our contract-library.com analysis infrastructure lets us do quickly.) On other chains, our search has not been as exhaustive, since we have no readily indexed repository of all deployed contracts. However, our best indicators suggest that there is no great exposure outside the AnySwap/Multichain contracts.

Concluding

We have been awarded Multichain’s maximum published bug bounty of $1M for each of the two vulnerability disclosures. (Thank you for the generous recognition of this extraordinary threat!)

This was an attack discovered by first suspecting the pattern and then looking for it in actual deployed contracts. Although in hindsight the attack vector is straightforward, it was far from straightforward when we first considered it. In fact, our initial exchange, at 2:30am on a Sunday, was literally:

“I had a crazy idea for a vulnerability. Want to sanity check the basics?”

Crazy, indeed, how this could lead to one of the largest hacks in history.

A few weeks ago, we were approached with a request to work on a project unlike any we’ve had before.

Cyrus Adkisson is the creator of Etheria, a very early Ethereum app that programmatically generates “tiles” in a finite geometric world. Etheria has a strong claim to being the first NFT project, ever! It was first presented at DEVCON1 and has been around since October 2015 — six years and counting. It is as much Ethereum “history” as can get.

Cyrus heard of us as bytecode and decompilation experts. His request was simple: try to reproduce the 6-yr old deployed bytecode of Etheria from the available sources. This is a goal of no small importance: Etheria tiles can be priced in the six digits and the history of the project can only be strengthened by tying the human-readable source to the long-running binary code.

Easy, right? Just compile with a couple of different versions and settings until the bytecode matches. Heck, etherscan verifies contracts automatically, why would this be hard?

Maybe for the simple fact that Cyrus had been desperately trying for months to get matching bytecode from the sources, to no avail! Christian Reitwiessner, the creator of Solidity and solc, had been offering tips. Yet no straightforward solution had been in sight, after much, much effort.

To see why, consider:

The version of solc used was likely (but not definitely) 0.1.6. Only one build of that version is readily available in modern tools (Remix) but the actual build used may have been different.

The exact version of the source is not pinned down with 100% confidence. The source code available was committed a couple of days after the bytecode was deployed.

Flags and optimization settings were not known.

The deployed code was produced by “browser-solidity”, the precursor of Remix. Browser-solidity is non-deterministic with respect to (we thought!) blank space and comments. (“Unstable” might be a better term: adding blank space seems to affect the produced bytecode. But we’ll stick with “non-deterministic”, since it’s more descriptive to most.)

If you want to try your hand at this, now is a good time to pause reading. It’s probably safe to say that after a few hours you will be close to convinced that this is simply impossible. Too many unknowns, too much unpredictability, produced code that is tantalizingly close but seemingly never the same as the deployed code!

Dead Ends

Our challenge consisted of finding source code or a compilation setup that would produce compiled code identical to the 6-yr old deployed Etheria bytecode.

The opening team message for the project set the tone: “We are all apprehensive but also excited about this project. It looks like a great mystery, but also a very hard and tedious search that will possibly fail.” Intellectual curiosity soon overtook all involved. People were putting aside their regular weekly assignments, working overtime to try to contribute to “the puzzle”. Some were going down a rabbithole of frantic searches for days — more on that later.

Some encouraging signs emerged at the very first look of the compiled code: when reverse-engineered to high-level code (by the lifter used in contract-library.com) it produced semantically identical Solidity-like output.

But our hopes were squashed upon more careful inspection. The low-level bytecode would always have small but significant differences. Some blocks were re-used (via jumps) in the deployed version but replicated (inlined) in the compiled version. The ordering of blocks would always be a little different. Even matching the bytecode size was a challenge: with manual tries of the (non-deterministic) compilation process, we would almost never get the deployed bytecode size down to the byte, always 2–4 bytes away.

Dead ends started piling up, but every one was narrowing the search space.

The version of solc used was definitely 0.1.6, based on the timeline of releases. However, the exact build might have made a difference. And, in fact, our compiler was not solc but solc-js, the Javascript wrapper of solc. There are 17 different versions of solc-js v0.1.6. There are even different versions with the exact same filename — e.g., there are 4 different builds (different md5 hashes) all called soljson-v0.1.6–2015–11–03–48ffa08.js. However, no optimizations or compilation gadgets that would explain the difference were introduced in the different builds. We could see no correlation between the compiled code artifacts and the exact build of solc-js, just the occasional non-determinism.

Different optimization settings made too-drastic a difference. Browser-solidity did not even allow configuring optimization runs, so the only question was whether optimization was on at all, and it very clearly was, based on the deployed bytecode.

Non-determinism seemed to creep in, even for changes as simple as the filename used.

With so little left to try, frustration started building up. Was this just a random search? And over what? Blank space in the compiled file? Reordering of functions? Small source code changes that yielded equivalent code? Removing dead code from the source?

We tried many of these, ad hoc or systematically and the tiny but persistent differences from the deployed bytecode never went away. Private function reordering looked very promising for a little while. But a full match was nowhere to be seen.

A Breakthrough

Although still several days away from the solution, an important insight arose, after lots of trial and error.

Non-determinism was due to solc-js, the Javacript wrapper, not to individual invocations of the solc executable itself. Solc-js is using emscripten to run the native solc executable inside a Javascript engine. Emscripten back in the day was translating a binary into asm.js (not yet WASM). Something in this pipeline was introducing non-determinism.

But what kind? Since the solc executable was itself deterministic when invoked freshly, the insight was that the apparent non-determinism of solc-js depended on what had been compiled before, and not only on no-op features of the compiled file (e.g., comments, blanks, filename)! In fact, we saw blank space in the compiled file rarely make a difference in the output bytecode. However, earlier compiled files reliably affected the later output.

Christian Reitwiessner later confirmed that non-determinism was due to using native pointers (i.e., machine addresses) as keys in data structures, so that a re-run from scratch was likely to appear deterministic (objects were being allocated to the same positions on an empty address space) whereas a followup compilation depended on earlier actions.

We now had a more reliable lever to apply force to and cause shuffles in the compiled bytecode. And we could get systematic — we would basically be fuzzing the compiler! Our workhorse was the functionality below, which you can try for yourself:

https://dedaub.com/etheria/fuzzer.html

Open the dev console on your browser (F12) and hit “go”. It starts compiling random (unrelated) files before it tries the main file we aim to verify. The (pseudo-)randomization process is controlled by a seed, so that if a match is found it can be reproduced. The seed gets itself updated pseudo-randomly and the process repeats. The output looks like this:

current seed 449777 automate.js:116:11

...

compile 0 NEW soljson-v0.1.6-2015-10-16-d41f8b7.js etheria-1pt2_nov4.sol(1968d2bc81cfd17cd7fd8bfc6cbc4672) 1700cdc5e2c5fbb9f4ca49fe9fae1291 -4 5796 automate.js:72:11

--------- NEW BEST ------------- 5796 1700cdc5e2c5fbb9f4ca49fe9fae1291

Notice the highlighted parts: this compilation output is “new” (i.e., not seen with previous seeds), has a length distance of -4 from the target, and an edit distance of 5796, which is a new best.

If you observe the execution, you can appreciate how much entropy is revealed: new solutions arise with high frequency, even many hours into the execution.

This got our team tremendously excited. Our channel got filled with reports of “new bests”. 0-605 (same size, edit distance 605) gave way to 0-261. We requisitioned our largest server to run tens of parallel headless browser jobs using selenium. The 0–261 record dropped to 0–150. On every improvement we thought “it can’t get any closer!” And with many parallel jobs running for hours, we let the server crunch for the night.

Finale

The next morning found the search no closer to the goal. 0–150 was derived from several different seeds. This is just a single basic block of 5 instructions in the wrong place, which also causes some jump addresses to shift. But still, not a zero.

By the next evening, it was clear that our fuzzing was running out of entropy. A little disheartened, we tried an “entropy booster” of last resort: adding random whitespace to the top and bottom of all compiled programs. (In fact, this improved-entropy version is the one at the earlier link.) Within hours, the “new best” became 0–114! And yet the elusive zero was still to be seen. Could it be that we would never find it?

Nearly 24 hours later, with the server fuzzing non-stop during the weekend, the channel lit up:

GUYS

WE GOT IT

All that was left was cleanup,tightening, and packaging. We soon had a solution that required merely compiling two unrelated files before the final compilation of the Etheria code. We repeated the process with the compiler running in multi-file mode. We found similar seeds for present-day Remix. Everything became streamlined, optimized, easy to reproduce and verify. You can visualize a successful verification (for one compiler setup) here:

https://dedaub.com/etheria/verify.html

We notified Cyrus a couple of hours later. It was great news, delivered on a Saturday, and the joy was palpable. We had a Tuesday advising call with Christian that was quickly repurposed to be a storytelling and victory celebration. Within a few days, etherscan verified the contract bytecode manually, since solc 0.1.6 is too old to be supported in the automated workflow.

Looking back, there are a few remarkable elements in the whole endeavor. The first is the amount of random noise amplified during a non-deterministic compilation. For a very long time, the sequence of “new” unique compiled bytecodes seemed never ending. A search that now seems, clearly, feasible appeared for long to be hopeless. Another interesting observation is how quickly people got wrapped up into a needle-in-a-haystack search. The challenge of a tough riddle does that to you. Or maybe it was some ancient magic from the faraway Etheria land?

We disclosed a critical bug to Harvest Finance. The contracts in scope held a total of $6.4M in Uniswap V3 positions. The attack was found by an automated analysis that attempted to generalize the elements of the OpenZeppelin UUPS uninitialized implementation vulnerability.

We present a static analysis approach that combines concrete values and symbolic expressions. This symbolic value-flow (“symvalic”) analysis models program behavior with high precision, e.g., full path sensitivity. To achieve deep modeling of program semantics, the analysis relies on a symbiotic relationship between a traditional static analysis fixpoint computation and a symbolic solver: the solver does not merely receive a complex “path condition” to solve, but is instead invoked repeatedly (often tens or hundreds of thousands of times), in close cooperation with the flow computation of the analysis.

The result of the symvalic analysis architecture is a static modeling of program behavior that is much more complete than symbolic execution, much more precise than conventional static analysis, and domain-agnostic: no special-purpose definition of anti-patterns is necessary in order to compute violations of safety conditions with high precision.

We apply the analysis to the domain of Ethereum smart contracts. This domain represents a fundamental challenge for program analysis approaches: despite numerous publications, research work has not been effective at uncovering vulnerabilities of high real-world value.

In systematic comparison of symvalic analysis with past tools, we find significantly increased completeness (shown as 83-96% statement coverage and more true error reports) combined with much higher precision, as measured by rate of true positive reports. In terms of real-world impact, since the beginning of 2021, the analysis has resulted in the discovery and disclosure of several critical vulnerabilities, over funds in the many millions of dollars. Six separate bug bounties totaling over $350K have been awarded for these disclosures.

The impact is not negligible, with a 26% gas cost increase on average. However, this will be gauged against the impact to the security and scalability of the consensus of the network, and Verkle trees could be a game-changer in this regard.

INTRODUCTION

Dedaub was commissioned by the Ethereum Foundation to investigate the impact of Vitalik Buterin’s Verkle tree gas metering proposal on existing smart contracts. In order to appraise the impact of the proposed change, we performed extensive simulations of the proposed changes over past transactions; wrote a static analysis and applied it over most contracts deployed to the mainnet; examined bytecode, source, decompiled code, and low level traces of past transactions.

Vitalik Buterin’s proposal introduces new gas changes to state access operations that closely reflect the worst case witness size that needs to be downloaded by a stateless client that needs to validate a block. As described in the original proposal, a Verkle tree is a cryptographically secure data structure with a high branching factor. Unlike Merkle trees, trace witnesses in Verkle trees do not need to include the siblings of each node in a path to the root node, which means that trees with a high branching factor are more efficient. Verkle trees can still retain the security properties by making use of a polynomial commitment scheme. By leveraging these properties, gas costs can therefore more easily reflect the upper bound of the cost of transmitting these witnesses across stateless clients, assuming these are appropriately designed.

In addition to gas changes that the proposal introduces, the Verkle tree proposal may break protocols that are too tied to the existing implementation, such as protocols that use Keydonix Oracles like Rune, but this consideration is outside the scope of this report.

In the report we briefly summarize the proposal with respect to gas costs. We then delve into the impact to existing contracts using two techniques: path-sensitive static program analysis, and dynamic analysis by modifying an Erigon node with the new gas semantics and analyzing the data per internal transaction. Finally we state our recommendations for lessening the impact of this proposal.

BACKGROUND

The goal of the proposal [1] aims to make Ethereum _stateless clients _sustainable in terms of data transmission requirements.

Stateless clients should be able to verify the correctness of any individual block without any extra information except for the block’s header and a small file, called witness, that contains the portion of the state accessed by the block along with proofs of correctness. Witnesses can be produced by any state-holding node in the network. The benefits of stateless verification include allowing clients to run in low-disk-space environments, enabling semi-light-client setups where clients trust blocks by default but stand ready to verify any specific block in the case of an alarm, and secure sharding setups where clients jump between shards frequently without the need to keep up with the state of all shards.

Large witness sizes are the key problem for enabling stateless clients for Ethereum and the adoption of Verkle trees can reduce the witness sizes needed. More specifically, a witness accessing an account in the hexary Patricia tree is, in the average case, close to 3 kB, and in the worst case it may be three times larger. Assuming a worst case of 6000 accesses per block (15m gas / 2500 gas per access), this corresponds to a witness size of ~18 MB, which is too large to safely broadcast through a p2p network within a 12-second slot. Verkle trees reduce witness sizes to ~200 bytes per account in the average case, allowing stateless client witnesses to be acceptably small.

Finally, contract code needs to be included in a witness. A contract’s code can contain up to 24000 bytes, and so a 2600 gas CALL can add ~24200 bytes to the witness size. This implies a worst-case witness size of over 100 MB. The proposal suggests breaking up contract code into chunks that can be proven separately; this can be done simultaneously with a move to a Verkle tree. Since a contract’s code can contain up to 24000 bytes, and so a 2600 gas CALL can add ~24200 bytes to the witness size. This implies a worst-case witness size of over 100 MB. The solution is to move away from storing code as a single monolithic hash, and instead break it up into chunks that can be proven separately and adding gas rules1 that accounts for these costs2.

The small witness sizes described above are possible because Verkle trees rely on an efficient cryptographic commitment scheme, called Polynomial Commitments34. Polynomial Commitments allow for logarithmic-sized (in respect to the tree’s height) proof-of-inclusion of any number of leaves in a subtree – and this is independent to the branching factor of the tree. In comparison, traditional Merkle tree’s proofs depend on the branching factor of the tree in a linear fashion, since all siblings of a node-to-be-proved must be included in the proof.

SUMMARY OF GAS CHANGES

The current proposal suggests new gas costs which have no counterpart in the previous versions of Ethereum. These is a gas cost for every chunk of 31 bytes of bytecode which are accessed and some additional access events that apply to the entire transaction. An improvement in gas cost can however be also achieved by lowering the cost for SLOAD/SSTORE for when fewer subtrees of the tree structure underpinning the state are accessed. The following is a summary of the gas cost changes between EIP-2929, which introduces the notion of “access lists” and the current proposal.

SLOAD, but location previously accessed within the same tx using SLOAD or SSTORE

Verkle

WARM_STORAGE_READ_COST (100)

EIP-2929

WARM_STORAGE_READ_COST (100)

SLOAD, but location previously unread within the tx using SLOAD or SSTORE

Verkle

200 if previously visited subtree 2100 if subtree has not been visited (storage location is up to 64 / 256 elements away from the closest visited)

EIP-2929

COLD_SLOAD_COST = 2100

CALL an address for an account that has not been previously accessed within the tx

Verkle

Access list costs (typically 1900 + 200 + 200 + more if value bearing)

EIP-2929

COLD_ACCOUNT_ACCESS_COST = 2600

EIP-2929 mentions that precompiles are not charged COLD_ACCOUNT_ACCESS_COST but the Verkle specification omits this case at the time of writing.

Last week we received bug bounties for disclosing smart contract vulnerabilities to Vesper Finance and BT Finance, via immunefi.com. Thank you, all!

(Notice for clients of these services: None of the vulnerabilities drain the original user funds. An attack would have financial impact, but not an overwhelming one. The maximum proceeds in the past few months would have been around $150K, and, once performed, the attack would be likely to alert the service to the vulnerability, making the attack non-repeatable. The vulnerabilities have since been mitigated and, to our knowledge, no funds are currently threatened.)

Both vulnerabilities follow the same pattern and many other services could potentially be susceptible to such attacks (though all others that we checked are not, by design or by circumstance — it will soon be clear what this means). It is, therefore, a good idea to document the pattern and draw some attention to it, as well as to its underlying financials.

Yield Skimming | The Attack

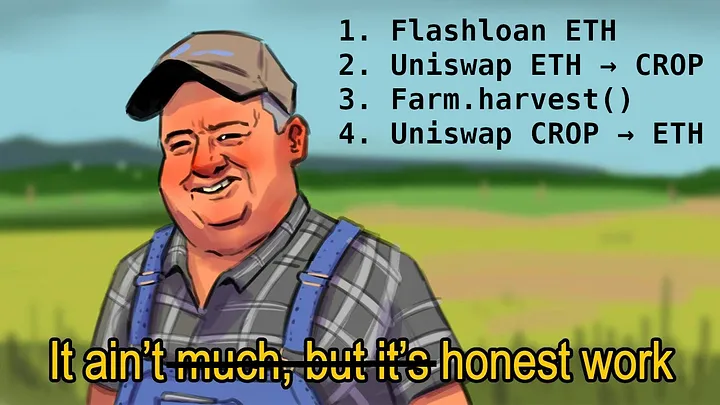

A common pattern in yield farming services is to have strategies that, upon a harvest, swap tokens on an exchange, typically Uniswap. A simplified excerpt from actual deployed code looks like this:

function harvest() public {

withdrawTokenA();

uint256 reward = TokenA.balanceOf(address(this));

unirouter.swapExactTokensForTokens(reward, 0, pathTokenAB, this, now.add(1800));

depositTokenB();

}

Example harvest function, with swapping.

Similar code is deployed in hundreds (if not thousands) of contracts. Typical uses of the pattern are a little more complex, with the harvest and the swap happening in different functions. But the essence remains unchanged. Similar code may also be found at the point where the service rebalances its holdings, rather than at the harvest point. We discuss harvest next, as it is rather more common.

[Short detour: you see that now.add(1800)for the “deadline” parameter of the swap? The add(1800) has no effect whatsoever. Inside a contract, the swap will always happen at time now, or not at all. The deadline parameter is only meaningful if you can give it a constant number.]

Back to our main pattern, the problem with the above code is that the harvest can be initiated by absolutely anyone! “What’s the harm?” — you may ask — “Whoever calls it pays gas, only to have the contract collect its rightful yield.”

The problem, however, is that the attacker can call harvest after fooling the Uniswap pool into giving bad prices for the yield. In this way, the victim contract distorts the pool even more, and the attacker can restore it for a profit: effectively the attacker can steal almost all of the yield, if its value is high enough.

In more detail, the attack goes like this:

a) the attacker distorts the Uniswap pool (the AssetA-to-AssetB pool) by selling a lot of the asset A that the strategy will try to swap. This makes the asset very cheap.

b) the attacker calls harvest. The pool does a swap at very bad prices for the asset.

c) the attacker swaps back the Asset B they got in the first step (plus a tiny bit more for an optimal attack) and gets the original asset A at amounts up to the original swapped (of step (a)) plus what the victim contract put in.

Yield Skimming | Example

For illustration, consider some concrete, and only slightly simplified, numbers. (If you are familiar with Uniswap and the above was all you needed to understand the attack, you can skip ahead to the parametric analysis.)

Say the harvest is in token A and the victim wants to swap that to token B. The Uniswap pool initially has 1000 A tokens and 500 B tokens. The “fair” price of an A denominated in Bs is 500/1000 = 0.5. The product k of the amounts of tokens is 500,000: this is a key quantity in Uniswap — the system achieves automatic pricing by keeping this product constant while swaps take place.

In step (a) the attacker swaps 1000 A tokens into Bs. This will give back to the attacker 250 B tokens, since the Uniswap pool now has 2000 A tokens and 250 B tokens (in order to keep the product k constant). The price of an A denominated in Bs has now temporarily dropped to a quarter of its earlier value: 0.125, as far as Uniswap is concerned.

In step (b) the victim’s harvest function tries to swap, say, 100 A tokens into Bs. However, the price the victim will get is now nowhere near a fair price. Instead, the Uniswap pool goes to 2100 A tokens and 238 B tokens, giving back to the victim just 12 B tokens from the swap.

In step (c) the attacker swaps back the 250 B tokens they got in step (a), or, even better, adds another 12 to reap maximum benefit from the pool skew. The pool is restored to balance at the initial 1000 A tokens and 500 B tokens. The attacker gets back 1100 A tokens for a price of 1000 A tokens and 12 B tokens. The attacker effectively got the 100 As that the victim swapped at 1/4th of the fair price.

Yield Skimming | Parametric Analysis

The simplistic example doesn’t capture an important element. The attacker is paying Uniswap fees for every swap they perform, at steps (a) and (c). Uniswap currently charges 0.3% of the swapped amount in fees for a direct swap. The net result is that the attack makes financial sense only when the amounts swapped by the victim are large. How large, you may ask? If the initial amount of token A in the pool is a and the victim will swap a quantity d of A tokens, when can an attacker make a profit, and what values x of A tokens does the attacker need to swap in step (a)? If you crunch the numbers, the cost-benefit analysis comes down to a cubic inequality. Instead of boring you with algebra, let’s ask Wolfram Alpha.

The result that Alpha calculates is that the attack is profitable as long as the number d of A tokens that the victim will swap is more than 0.3% of the number a of A tokens that the pool had initially. In the worst case, d is significant (e.g., 10% of a, as in our example) and the attacker’s maximum profit is very close to the entire swapped amount.

Another consideration is gas prices, which we currently don’t account for. For swaps in the thousands of dollars, gas prices will be a secondary cost, anyway.

Yield Skimming | Mitigation

In practice, yield farming services protect against such attacks in one of the following ways:

They limit the callers of harvest or rebalance. This also needs care. Some services limit the direct callers of harvest but the trusted callers include contracts that have themselves public functions that call harvest.

They have bots that call harvest regularly, so that the swapped amounts never grow too much. Keep3r seems to be doing this consciously. This is fine but costly, since the service incurs gas costs even for harvests that don’t produce much yield.

They check the slippage suffered in the swap to ensure that the swap itself is not too large relative to the liquidity of the pool. We mention this to emphasize that it is not valid protection! Note the numbers in our above example. The problem with the victim’s swap in step (b) is not high slippage: the victim gets back 12 B tokens (11.9 to be exact) whereas with zero slippage they would have gotten back 12.5. This difference, of about 5%, may certainly pass a slippage check. The problem is not the 5% slippage but the 4x lower-than-fair price of the asset, to begin with!

There are other factors that can change the economics of this swap. For instance, the attacker could be already significantly vested in the Uniswap pool, thus making the swap fee effectively smaller for them. Also, Uniswap v3 was announced right at the time of this writing, and promises 0.05% fees for some price ranges (i.e., one-sixth of the current fees). This may make similar future attacks a lot more economical even for small swaps.

Conclusion

The pattern we found in different prominent DeFi services offers opportunities for interesting financial manipulation. It is an excellent representative of the joint code analysis (e.g., swap functionality reachable by untrusted callers) and financial analysis that are both essential in the modern Ethereum/DeFi security landscape.

Following the previous white-hat hacks (1, 2), on contracts flagged by our analysis tools, today we’ll talk about another interesting contract. It’s hackable for about $80K, or rather its users are: the contract is just an enabler, having approvals from users and acting on their commands. However, a vulnerability in the enabler allows stealing all the users’ funds. (Of course, we have mitigated the vulnerability before posting the article.)

The vulnerable contract is a sophisticated arbitrage bot, with no source on Etherscan. Being an arbitrage bot, it’s not surprising that we were unable to identify either the contract owner/deployer or its users.

One may question whether we should have expended effort just to save an arbitrageur. However our mission is to secure the smart contract ecosystem — via our free contract-library service, research, consulting, and audits. Furthermore, arbitrage bots do have a legitimate function in the Ethereum space: the robustness of automated market makers (e.g., Uniswap) depends on the existence of bots. By having bots define a super-efficient trading market, price manipulators have no expected benefit from biasing a price: the bots will eat their profits. (Security guaranteed by the presence of relentless competition is an enormously cool element of the Ethereum ecosystem, in our book.)

Also, thankfully, this hack is a great learning opportunity. It showcases at least three interesting elements:

Lack of source code, or general security-by-obscurity, won’t save you for long in this space.

There is a rather surprising anti-pattern/bad smell in Solidity programming: the use of this.function(...) instead of just function(...).

It’s a lucky coincidence when an attack allows destroying the means of attack itself! In fact, it is the most benign mitigation possible, especially when trying to save someone who is trying to stay anonymous.

Following a Bad Smell

The enabler contract has no source code available. It is not even decompiled perfectly, with several low-level elements (e.g., use of memory) failing to be converted to high-level operations. Just as an example of the complexity, here is the key function for the attack and a crucial helper function (don’t pay too close attention yet — we’ll point you at specific lines later):

Faced with this kind of low-level complexity, one might be tempted to give up. However, there are many red flags. What we have in our hands is a publicly called function that performs absolutely no checks on who calls it. No msg.sender check, no checks to storage locations to establish the current state it’s called under, none of the common ways one would protect a sensitive piece of code.

And this code is not just sensitive, it is darn sensitive. It does a delegatecall (line 55) on an address that it gets from externally-supplied data (line 76)! Maybe this is worth a few hours of reverse engineering?

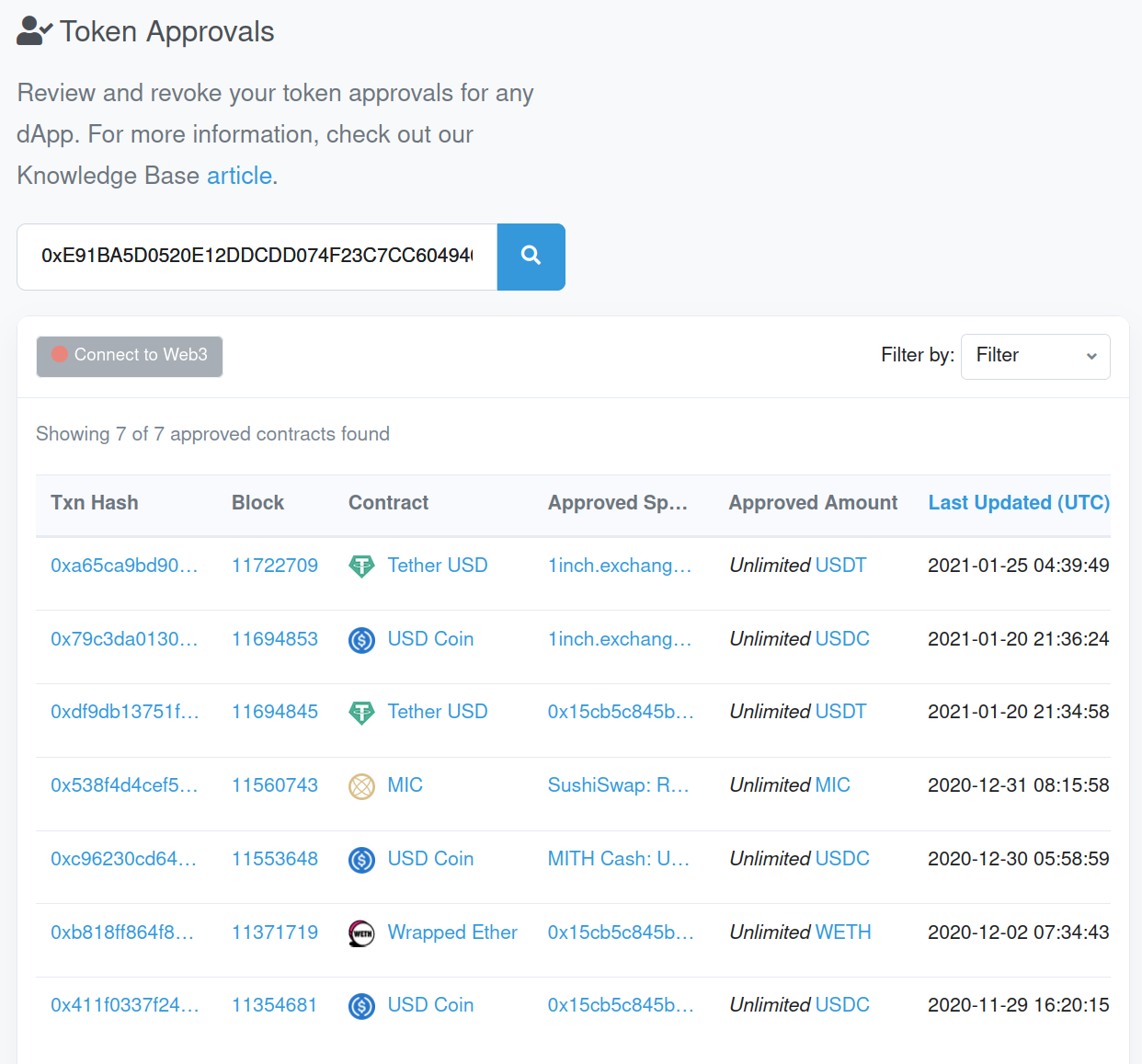

Vulnerable code in contracts is not rare, but most of these contracts are not used with real money. A query of token approvals and balances shows that this one is! There is a victim account that has approved the vulnerable enabler contract for all its USDT, all its WETH, and all its USDC.

Victim token approvals, including to the enabler (0x15cb5c845b…).

And how much exactly is the victim’s USDT, USDC, and WETH? Around $77K at the time of the snapshot below.

Victim’s balances.

Reverse Engineering

The above balances and suspicious code prompted us to do some manual reverse engineering. While also checking past transactions, the functionality of the vulnerable code was fairly easy to discern. At the end of our reverse-engineering session, here’s the massaged code that matters for the attack:

pragma experimental ABIEncoderV2;

contract VulnerableArbitrageBot is Ownable {

struct Trade {

address executorProxy;

address fromToken;

address toToken;

...

}

function performArbitrage(address initialToken, uint256 amt, ..., Trade[] trades memory) onlyOwner external {

...

IERC20(initialToken).transferFrom(address(this), amt);

...

this.performArbitrageInternal(..., trades); // notice the use of 'this'

}

function performArbitrageInternal(..., Trade[] trades memory) external {

Trade memory trade = trades[i];

for (uint i = 0; i < trades.length; i++) {

// ...

IERC20(trade.fromToken).approve(...);

// ...

trades[i].executorProxy.delegatecall(

abi.encodeWithSignature("trade(address,address...)", trade.fromToken, trade.toToken, ...)

);

}

}

}

interface TradeExecutor {

function trade(...) external returns (uint) {

}

contract UniswapExecutor is TradeExecutor {

function trade(address fromToken, address toToken, ... ) returns (uint) {

// perform trade

...

}

}

This function, 0xf080362c, or performArbitrageInternal as we chose to name it (since the hash has no publicly known reversal), is merely doing a series of trades, as instructed by its caller. Examining past transactions shows that the code is exploiting arbitrage opportunities.

Our enabler is an arbitrage bot and the victim account is the beneficiary of the arbitrage!

Since we did not fully reverse engineer the code, we cannot be sure what is the fatal flaw in the design. Did the programmers consider that the obscurity of bytecode-only deployment was enough protection? Did they make function 0xf080362c/performArbitrageInternal accidentally public? Is the attack prevented when this function is only called by others inside the contract?

We cannot be entirely sure, but we speculate that the function was accidentally made public. Reviewing the transactions that call 0xf080362c reveals that it is never called externally, only as an internal transaction from the contract to itself.

The function being unintentionally public is an excellent demonstration of a Solidity anti-pattern.

Whenever you see the code pattern <strong>this.function(...)</strong> in Solidity, you should double-check the code.

In most object-oriented languages, prepending this to a self-call is a good pattern. It just says that the programmer wants to be unambiguous as to the receiver object of the function call. In Solidity, however, a call of the form this.function() is an external call to one’s own functionality! The call starts an entirely new sub-transaction, suffers a significant gas penalty, etc. There are some legitimate reasons for this.function() calls, but nearly none when the function is defined locally and when it has side-effects.

Even worse, writing this.function() instead of just function() means that the function has to be public! It is not possible to call an internal function by writing this.function(), although just function() is fine.

This encourages making public something that probably was never intended to be.

The Operation

Armed with our reverse-engineered code, we could now put together attack parameters that would reach the delegatecall statement with our own callee. Once you reach a delegatecall, it’s game over! The callee gains full control of the contract’s identity and storage. It can do absolutely anything, including transferring the victim’s funds to an account of our choice.

But, of course, we don’t want to do that! We want to save the victim. And what’s the best way? Well, just destroy the means of attack, of course!

So, our actual attack does not involve the victim at all. We merely call selfdestruct on the enabler contract: the bot. The bot had no funds of its own, so nothing is lost by destroying it. To prevent re-deployment of an unfixed bot, we left a note on the Etherscan entry for the bot contract.

To really prevent deployment of a vulnerable bot, of course, one should commission the services of Dedaub. 🙂